How shall the Energy Efficiency First principle be applied in the hydrogen economy?

11 September 2023

How are high tax reductions (tax relief) justified by the public benefits of private energy efficiency investment?

12 September 2023

By Emma Schwentner

In the face of climate change and the energy transition, energy efficiency has become a crucial goal for governments, businesses, and individuals. However, the business objective of selling energy usually runs contrary to the act of saving energy. White certificate schemes are one market-based mechanism to address this market failure.

In essence a ‘white certificate’ (WhC) represents a unit of energy saved. Usually, certificates are issued by government agencies for specific implemented projects which could for example include infrastructure renovation, but also large-scale changing of light bulbs. Depending on the specific scheme these projects can be carried out by Energy suppliers, distributors, ESCOs or even companies themselves. To create an incentive for the creation of white certificates, governments set energy savings targets on energy suppliers or distributors, which at the end of a period must own a certain number of white certificates. This creates a market demand for energy savings -as it artificially introduces scarcity – and in theory provides a flexible mechanism to meet energy savings targets at the lowest aggregate cost (Di Santo, D., & Biele, E, 2017).

While there are more than fifty energy obligation systems generating certificates in place all over the world, most of them do not have marketplaces or trading schemes and market design proves to be challenging (IEA, 2020). The following paper examines the market mechanism of the scheme in detail, focusing particularly on the price formation, as their price can determine whether an energy investment might be profitable (Perrels, 2008). The objective is to explore the price formation in white certificate markets using different approaches. Theoretical models are used to gain an understanding of the underlying mechanisms of these markets. In addition, empirical results are used to provide insights into the practical aspects of white certificates, with particular emphasis on the comparison of the three European countries that have introduced white certificates: Italy, France, and the UK. Price developments in the Italian and French markets since 2014 are examined in more detail, especially with regards to policy interventions. By combining theoretical and empirical findings, this paper aims to provide a comprehensive analysis of price formation in white certificate markets.

Modelling White Certificate Markets

The white certificate market is a relatively new and complex system, therefore theoretical models are a good first step to identify the key drivers of prices and their interactions. While traditional factors such as supply and demand are relevant, they may not be sufficient to explain the price dynamics in the white certificate market.

Perrels 2008 Model

To provide a more detailed understanding of price building the following section will introduce a model developed by Perrels (2008), which illustrates key factors regarding price formation. It is based on several key assumptions:

- The existence of an identifiable savings potential within the energy system.

- The existence of ‘scarcity’, reasonably set targets which create a demand for white certificates.

- The absence of credibility issues, certificates represent actual energy savings, no issues related to additionality.

- Energy Efficiency Investment choices are based on end use energy price, unit cost and potential of savings as well as the price of white certificates.

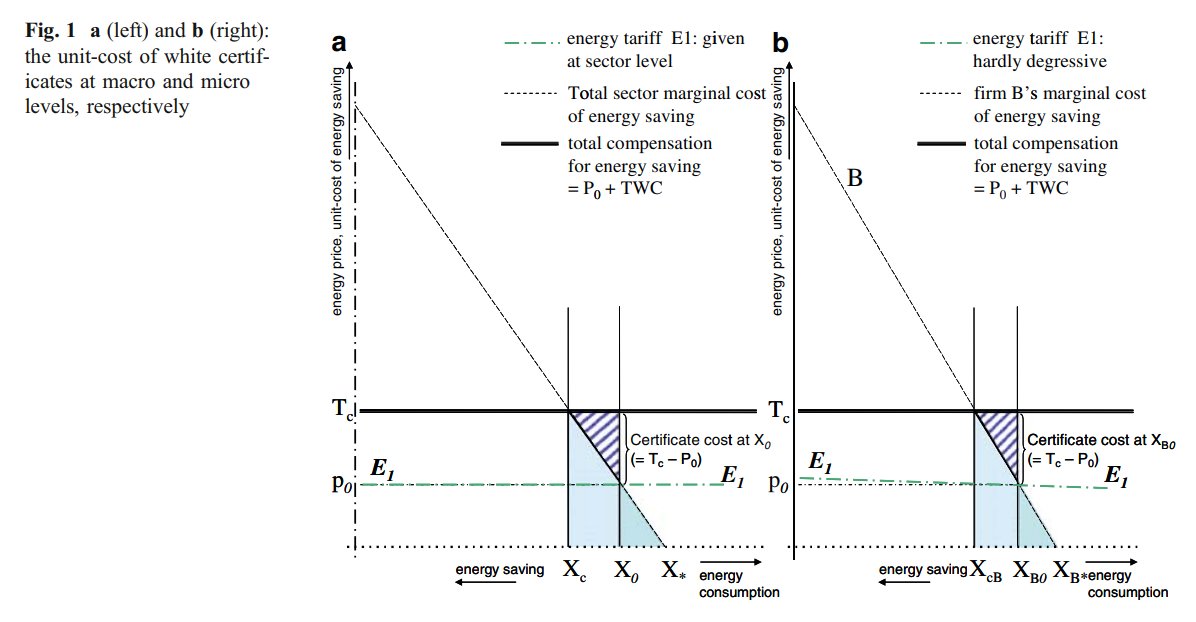

This allows the following model to be set up, where the horizontal axis represents energy consumption while the vertical axis simultaneously depicts unit costs of energy savings and energy prices. The initial consumption before the implementation of a WhC scheme is at X0, where the marginal cost of saving energy is equal to the energy price. After implementation, the consumption must shift to Xc, the government set target consumption, resulting in the increase of marginal cost of energy savings to Tc. Assuming a smoothly functioning market, the price of the certificate will then be equal to the difference between the marginal cost of energy saving Tc and the energy price. Therefore, in a well-functioning market the unit-cost of a marginal energy savings as well as the overall saving target are important determinants of the price of certificates (Perrels, 2008).

One can further consider the situation of a firm B in a sector included in the white certificate scheme modelled in Figure 1(a), where it is assumed that the obligated party will reimburse firm B an amount equal to the value of the white certificates that will be transferred. Firm B pays an energy price equivalent to the sector’s average, and since the certificate price, which steers the exploitation of the firm’s energy savings potential, is exogenous to firm B, the total compensation level Tc of the sector also applies for firm B. Therefore, as a result Firm B consumption would move to XcB. The firm can cut costs and sell the effort to the obligated party at price Tc-p0, ending up with net benefits. For a higher energy price, the saving would be the same while the overall net benefits. (Perrels, 2008)

This simple set up illustrates that in a well functioning market, the unit-cost of a marginal energy savings, as well as the overall savings target are important determinants of the price of certificates (Perrels, 2008). It clarifies the business case of white certificate sales. Perrels (2008) then expands on this model and uses it to analyse price reactions to different factors, for example interplay with other policies, which has also been analysed by other authors (Oikonomou et al., 2008). The main result is that more ambitious energy savings targets and more heterogeneous unit costs and end prices lead to higher market liquidity and market efficiency.

Oligopolistic market models

Another important theoretical model treats white certificate markets as an oligopolistic market with a market leader (Oikonomou et al., 2008). This is particularly interesting as oligopolistic markets are closer to reality, for example in Italy one distributor had 50% of total compliance obligations (Pela, A., 2015). Oikonomou et al. finds that the market leader supplies larger quantities of certificates and can sell at lower prices. Placing high targets on the leading company therefore leads to lower WhC prices, which in turn can help overcome market barriers but might also push smaller companies out of the market. (Oikonomou et al., 2012) White certificate schemes potentially giving a competitive disadvantage to market newcomers is something often pointed by opponents to the scheme. Yet, while there is a theoretical possibility for abuse, Crampes (2020) points out that so far, no such situations arose in certificate markets.

Insights into Market Liquidity, Volatility, and Interventions in White Certificate Trading

The previous section provided some purely theoretical factors affecting the price formation on white certificate markets, much of it depending on market liquidity. However, trade is actually very low in most white certificate schemes (Giraudet & Finon, 2015). Therefore, this empirical section aims to examine the actual market performance of three white certificate schemes in Europe: Italy, France, and the UK. The focus is on understanding policy interventions impacting prices as well as factors which increase market liquidity.

The Italian scheme has been put in place in 2005 and has the most extensive certificate market, trading is a central aspect of the mechanism. Energy savings obligations are put on energy distributors, who can acquire WhC by implementing projects themselves, trading bilaterally or on a monitored spot market monitored by a government agency (GME, 2023). This trading platform has pre-set rules, guaranteeing transparency and security of market deals. In the first 3 years of the scheme, the traded volume of WhC corresponds to around 120% of national targets (Eyre et al., 2009) and 75% of issued white certificates were involved in some kind of trading (Giraudet & Finon, 2015).

In France, a white certificate scheme exists since 2006 and while there has been some trading, the market is by far not as important as in Italy. Obligations are placed on energy suppliers who seem to prefer to implement the projects themselves. While other eligible actors could participate, trading occurs between obligated parties via bilateral trades (IEA, 2022). In the first 2 years of the scheme only 1.5% of delivered white certificates, with value of 1.4 M Euro have been traded (Eyre et al., 2009) and the amount of white certificates traded was lower than 4% of France total obligation (Bertoldi et al., 2010).

In the UK, energy efficiency obligations for suppliers have been in place since 2002. Legislation allows for trading, but there is no transparent market and while some trade is suspected, it is believed to be negligible. (Eyre et al., 2009; Giraudet & Finon, 2015)

Market Liquidity

Market liquidity is essential for efficient price building of white certificate markets, however there are few white certificate markets with high levels of trading activity. This is partially due to the nature of the mechanism markets and can be explained theoretically, for example, markets unlikely to be liquid in the beginning, as credits are available for sale only once the target is met. Furthermore, low compliance costs can lead obligated parties to prefer to implement projects themselves, to protect market share and prevent competitors from gaining strategic information. (Giraudet & Finon, 2015) Also, heterogeneous compliance costs are a necessity for trade to arise (Newell & Stavins, 2003).

The level of trade in the Italian white certificate scheme is much higher than in France and the UK, comparing between these three systems makes some tentative empirical considerations about fostering trade in white certificate markets possible. However, much more econometric analysis, experience and data would be necessary for these results to solidly demonstrate a causality. This research and data gap has already been pointed out, yet prevails, partially due to the market nature of the mechanism, as participants might be reluctant to share information (Giraudet & Finon, 2015).

Information and transparency are also factors that lead to higher market liquidity. Unlike the French and UK markets, Italy has a well-established trading platform and public availability of WhC prices, which promotes transparency and price certainty (Pela, A., 2015). In addition, the market share distribution of energy distributors in Italy, which operate as an oligopoly with a dominant market leader, possibly leads to higher cost heterogeneity, which is necessary for horizontal trade. The most important factor leading to significantly higher trade in Italy seems to be that obligated parties are energy distributors, which incentivizes vertical trade and creates a market for energy service companies (ESCOs) to develop and deliver energy-saving projects(Giraudet & Finon, 2015).

Comparing price changes

Comparing prices on different markets can be challenging due to different units and general difference in market design. The graph in Figure 2 illustrates the change in white certificate prices in France and Italy, it is indexed with base year set in 2014. The upward price trend in France indicates that the projects with higher costs are becoming more prevalent, as easier-to-achieve, low-hanging fruit projects such as bulk light bulb replacements have already been implemented extensively. However, relative price stability in France comparing to other schemes points to a maturing of the market design and should be investigated further.

Generally, price volatilities have sometimes been a result of policy makers making corrective interventions to invest or limit costs to consumers. For example, in 2017 Italy tightened eligibility criteria and the resulting shortage of white certificates increased prices drastically, after having been stable for more than five years (Di Santo, D., & Biele, E, 2017). Modifying the criteria for qualifying projects has also led to price changes in other countries (IEA, 2020). This is in line with previously discussed theoretical results, as it changes potential for savings and hence with equal targets the share increases and also might directly disincentivise trading (Bertoldi & Rezessy, 2009). In response to the peak in prices, Italy introduced a price cap in 2018 to provide some stability, with prices never falling far below it since.

Floor and ceiling prices

Clearly, one way for policy makers to provide price stability or steer the price is to set floor and ceiling prices. The idea behind a floor price is that it prevents prices from falling too low, which could disincentivise investment. Although no European country has implemented a floor price, some WhC-schemes, like the one in Connecticut, have done so (Aldrich & Koerner, 2018). Meanwhile, a ceiling price is intended to prevent prices from becoming too high. Next to setting a price cap like Italy, a non-compliance penalty also effectively caps the price of certificates. France’s white certificate prices are therefore effectively capped due to the penalty, this however allows for buy-out. Italy and the UK have chosen to forego penalties in order to avoid a buy-out price (Bertoldi & Rezessy, 2009).

Conclusion

In conclusion, trade in the European white certificate schemes is generally low and while certificate prices remain relatively volatile. Despite their importance for the schemes, data on prices is scarce and therefore good research results are limited. This text highlighted the significance of several factors. Firstly, the savings targets set by regulatory authorities play a crucial role in determining the price of certificates in a well-functioning market. Moreover, who these targets are placed on makes a significant difference. Placing high targets on the leading company in an oligopolistic market can result in lower white certificate prices. Market liquidity, influenced by factors such as cost heterogeneity and eligibility criteria, also plays a significant role. While some conclusions about price building can be drawn by considering models and combining theoretical and empirical insights, the exact price formation on white certificate markets remains elusive. Exploring the impact of different market design features on prices and market efficiency should remain a priority for future research.

Bibliography

Aldrich, E. L., & Koerner, C. L. (2018). White certificate trading: A dying concept or just making its debut? Part I: Market status and trends. The Electricity Journal, 31(3), 52–63. https://doi.org/10.1016/j.tej.2018.03.002

Bertoldi, P., & Rezessy, S. (2009). Energy saving obligations and tradable white certificates (JRC Science and Policy Reports) [JRC59129].

Bertoldi, P., Rezessy, S., Lees, E., Baudry, P., Jeandel, A., & Labanca, N. (2010). Energy supplier obligations and white certificate schemes: Comparative analysis of experiences in the European Union. Energy Policy, 38(3), 1455–1469. https://doi.org/10.1016/j.enpol.2009.11.027

Crampes, C., & Léautier, T.-O. (n.d.). White certificates and competition. TSE Working Papers, 20–1167. https://ideas.repec.org/p/tse/wpaper/124950.html

Di Santo, D., & Biele, E. (2017). The Italian white certificates scheme. Case study prepared by FIRE for the EPATEE project, funded by the European Union’s Horizon 2020 programme.

Eyre, N., Pavan, M., & Bodineau, L. (2009). Energy company obligations to save energy in Italy, the UK and France: What have we learnt? ECEEE 2009 Summer Study Act! Innovate! Deliver! Reducing Energy Demand Sustainably, 429–439.

Giraudet, L.-G., & Finon, D. (2011). White certificate schemes: The static and dynamic efficiency of an policy instrument.

Giraudet, L.-G., & Finon, D. (2015). European experiences with white certificate obligations: A critical review of existing evaluations. Economics of Energy & Environmental Policy, 4. https://doi.org/10.5547/2160-5890.4.1.lgir

GME. (2023). Gestore Mercati Energetici. https://www.mercatoelettrico.org/En/Statistiche/TEE/StatisticheTEE.aspx

IEA. (2020). World Energy Investment 2020. https://www.iea.org/reports/world-energy-investment-2020

IEA. (2022, March 29). White Certificate Scheme & Obligation – Policies. IEA. https://www.iea.org/policies/1854-white-certificate-scheme-obligation

Newell, R. G., & Stavins, R. N. (2003). Cost Heterogeneity and the Potential Savings from Market-Based Policies. Journal of Regulatory Economics, 23(1), 43–59. https://doi.org/10.1023/A:1021879330491

Oikonomou, V., Di Giacomo, M., Russolillo, D., & Becchis, F. (2012). White Certificates in the Italian Energy Oligopoly Market. Energy Sources, Part B: Economics, Planning, and Policy, 7(1), 104–111. https://doi.org/10.1080/15567240902839286

Oikonomou, V., Jepma, C., Becchis, F., & Russolillo, D. (2008). White Certificates for energy efficiency improvement with energy taxes: A theoretical economic model. Energy Economics, 30, 3044–3062. https://doi.org/10.1016/j.eneco.2008.04.005

Pela, A. (2015). The Italian White Certificate Scheme: Cost of EEO Scheme and Cost Recovery Mechanism. Gestore Servizi Energetici (GSE). http://enspol.eu/sites/default/files/The%20Italian%20White%20Certificate%20Scheme%2C%20Alberto%20Pela%20%E2%80%93%20GSE.pdf

Perrels, A. (2008). Market imperfections and economic efficiency of white certificate systems. Energy Efficiency, 1(4), 349–371. https://doi.org/10.1007/s12053-008-9020-z