The US Inflation Reduction Act: Is it a Green Deal?

25 March 2025

By Talip AYDIN, Costanza GALETTO, Joseph JONA FALCO, Arno MINASIAN, Leon RENNER & Emma SEGRÈ

Introduction

Launched in December 2019 by the European Commission, The European Green Deal (EGD) serves as a transformative framework to address the challenge of climate change, fundamentally affecting and reshaping Europe’s geopolitical and energy landscape. Crucially, as Europe transitions away from harmful fossil fuels dependencies towards a more sustainable and diversified energy mix – an imperative further underscored by the geopolitical challenges following the Russian invasion of Ukraine – new dependencies are emerging. In fact, while the EU is currently attempting to secure new short and medium-term gas supplies that are necessary in this transitory phase, it is also evident that in the longer run the complete phase out of oil and gas may lead to the emergence of new vulnerabilities that should be carefully assessed and anticipated. Simultaneously, as the EU attemps to decouple from unreliable energy partners, it also seeks to act as a leader in the global green transition – driven by both necessity and strategic advantage.

Against this background, the present contribution aims to investigate the geopolitical elements embedded in the EU’s strategy towards climate neutrality, by asking the question “to what extent does the EGD lead to a shift in the dependencies and geopolitical strategies of the EU?”. Importantly, we will thus limit the scope of our investigation to the EGD’s geopolitical impact for the EU and third countries, not considering the potential interconnected effects of other Green Deals or related policies adopted by different actors – such as the IRA (US), the Green New Deal (South Korea), or the 14th Five-Year Plan for Ecological and Environmental Protection (China).

Accordingly, it will be argued that while the EGD cannot fully free the EU from external dependencies, it compels a deliberate shift towards new, strategically managed, and diversified dependencies. Concurrently, it will also be shown that the EGD aims to position the EU as a global leader in the green transition, enhancing its economic and diplomatic influence.

Literature Review

Since the adoption of the EGD, several studies have investigated the potential geopolitical dynamics embedded within it [1],[2],[3]. Leonard et al., in 2021 – hence before the 2022 Russian war of aggression against Ukraine – already assessed in the potential geopolitical effects following from this strategy, anticipating the need to mitigate its negative impacts on partner countries while securing raw materials [4]. Later, this has been further reinforced by Bolduc et al. (2022) and Marhold (2023) in the face of the war [5],[6]. The latter in fact has ultimately created the required momentum for the move towards what Marhold (2023) refers to as a “security-centered” decarbonization strategy, namely one that is premised on “security first, compliance [with trade rules] second” [7]. A variety of studies then have scrutinized more closely the potential emergence of new dependencies due to the green transition, focusing on the role of hydrogen as well as critical raw materials more in general [8], [9]. Meanwhile, Bjerkem et al. (2020) have focused on the potential strategic importance of European standardization through the enhancement of the EGD [10]. This perspective has also been elaborated – though with a much more negative and critical stance – by Almeida et al. (2023), who reflect on the “colonial structures of power” that in their view are inherent in such engagement of the EU in green diplomacy, trade, and investment [11].

Against this backdrop, our contribution aims to synthesize these discussions by tracing the historical and emerging dependencies tied to the EGD’s decarbonization strategy, while also assessing its potential to position the EU as a global standard setter in climate governance.

I. Shifting Dependencies

Historic Dependencies: A Fragile Foundation

For the past three decades, Europe’s economic stability and industrial growth have been deeply intertwined with the import of external energy sources [12]. In particular, from the 1990s onwards, in parallel to the on-going liberalization of the internal energy market, EU countries gradually started to recognize the potential benefits of incorporating former socialist and Soviet countries into the European energy framework [13]. This approach was shaped by the success of Germany’s ‘Wandel durch Handel’ doctrine—”change through trade”—which largely defined the EU’s energy relations with Russia until the invasion of Ukraine [14]. Major projects like controversial Nord Stream I and II emerged from this policy, despite early signs of the risks associated with such dependence. Likewise, the EU27 have historically greatly relied on autocratic petrostates for the supply of oil and gas, whose main source of revenue are fossil fuels. Again, although there have been signs of risks – such as in 2011 with the uprising against the regime of Gaddafi and the consequent oil supply shock – little action was taken to address this fragility [15].

As a result of this trend, in 2021, Russia supplied more than 40% of the gas consumed by the EU, along with 46% of its coal and 27% of its oil [16]. Moreover, the Energy Import Dependency of the EU27 – defined by Eurostat as the proportion of energy a country must import to fulfill its overall energy requirements – amounted to around 60% [17].

Ultimately, the vulnerability of this framework came to the surface with the unprecedented crisis caused by the Russian war of aggression against Ukraine in 2022. As Moscow weaponized gas exports and the EU struggled to secure alternative fossil fuel suppliers—further complicated by production cuts from the Organization of the Petroleum Exporting Countries—EU policymakers were forced to confront the issue of excessive dependence on external energy sources [18].

Seeking to diversify the energy supply and quickly roll-out the deployment of renewables, the EGD is indeed a promising path for the EU to decouple its economic growth from the supply of energy from undemocratic and unstable countries [19]. By now, the green transition is thus seen as the sole path towards ensuring “secure, sustainable and affordable energy worldwide” [20]. This notwithstanding, there are clear pitfalls in believing that the green transition will create energy security in the EU per se. In fact, as it will be shown in the next sections, new external dependencies may arise, particularly in the context of the supply of critical raw materials and new technologies which are indispensable for the transition.

Navigating Short-Term Challenges: The Role of Gas and Oil

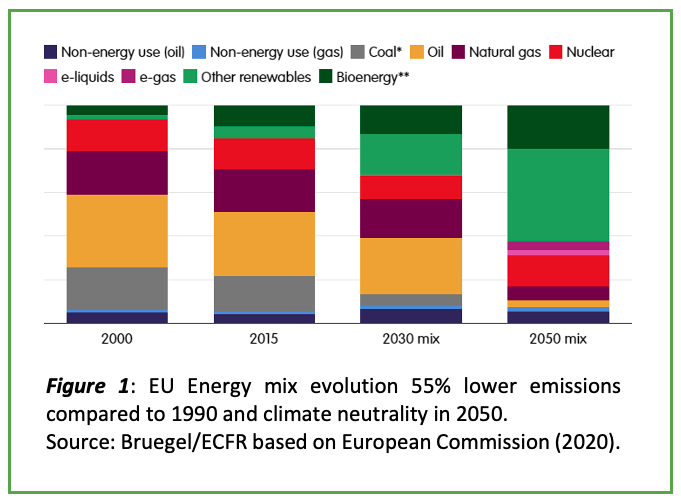

In the following section, the new short-term challenges arising from the current geopolitical tensions will be briefly assessed. In fact, as shown by Figure 1, despite the EU carbon neutrality goals, during the initial transitional phase towards the EU’s 2030 targets, gas and oil remain vital energy sources. However, according to the EGD plan, by 2050, oil will be nearly phased out, and gas will account for less than 10% of the EU’s energy needs [21], [22].

In the meantime, however, to meet Europe’s ongoing demand for oil and gas, in 2022 the EU Commission launched the REPowerEU Plan. This initiative was developed to reduce reliance on Russian fossil fuel imports by focusing on energy savings, diversifying sources, and boosting clean energy production.

Through REPowerEU, the EU has mitigated energy shortages, supported Ukraine by reducing Russian revenue, stabilized energy prices, and achieved milestones such as an 18% reduction in gas consumption, breaking dependency on Russian imports, increasing renewable energy installations, and surpassing gas with wind and solar electricity production for the first time [23].

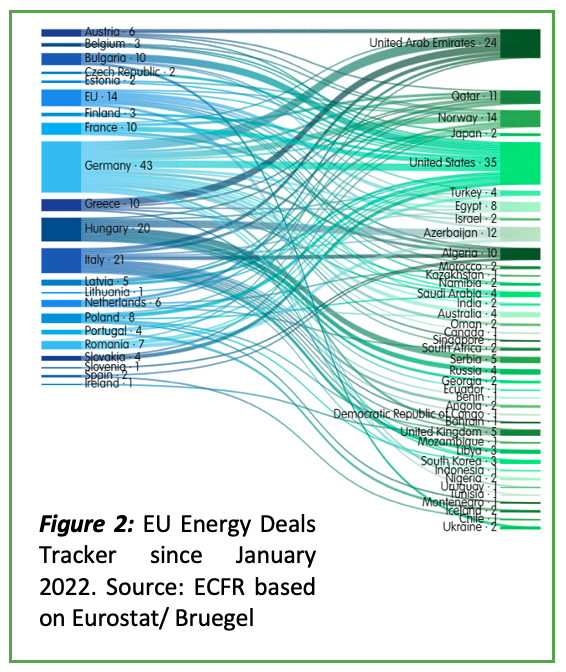

However, as pictured by Figure 2, with the cessation of imports from Russia, the EU prioritized securing alternative gas supplies in the short and medium term, broadening and diversifying its range of suppliers. Of the 183 new agreements made since January 2022, approximately half involve gas or liquefied natural gas (LNG) [24]. Importantly, despite the emphasis on joint fuel purchases to avoid competition among Member States, the EU has yet to achieve the desired economies of scale [25], [26].

Member States have in fact also engaged in several bilateral agreements with countries such as Algeria, UAE, Qatar, and the United States, impacting long-term infrastructure planning. About half of these energy deals involve clean energy as well, showcasing varying levels of commitment, from exploring renewable sources to infrastructure development, reflecting the urgent need to invest in clean energy for sustainable decarbonization.

Hence, it is important to consider the serious consequences for new or reinforced oil and gas partners exporting to the EU, especially in the European Neighborhood. This is the case especially North Africa, accounting for 14.1% of European gas imports in 2023, as well as Azerbaijan, which has increased oil-exports to the EU under a Memorandum of Understanding in 2022 [27]. Currently, 90% of its total exports concern oil, of which more than 70% goes to the EU [28].

According to Leonard et al. (2021), this means that the EU has the possibility and leverage to actively promote a proper green transition in these countries to ensure that long-term repercussions of the EGD will not cause an unstable European Neighborhood [29].

Paving the Way for the Future: The Promise of Hydrogen

Aside from the short-term shifts in dependencies, the EU remains focused on its objectives of phasing out gas and oil in the medium and long term. As part of this endeavor, green hydrogen is likely to play a substantial part. Its deployment will be crucial for hard-to-abate industries (e.g., steel and cement) and heavy transports (e.g., aviation and long-distance shipping), i.e., sectors where electrification is not a viable short-term option [30].

Since Europe lacks sufficient renewable energy to produce green hydrogen en masse [31] –as it is won via the electrolysis of water, which requires a considerable renewable energy input– its procurement through imports gives rise to questions about the geopolitical issues at stake. In the following we will briefly tackle the potential dependencies that may arise from this, the implications for the EU’s neighborhood, and the role for industrial policy.

Firstly, given the fact that hydrogen can be produced virtually everywhere, its market should not be characterized by the same level of “cartelization” as the trade in fossil fuels [32].

Despite the likelihood of traditional fossil fuel-producing states modifying their industries towards greater prominence of hydrogen to evade a decline in geopolitical influence, the heightened strategic awareness in Europe, especially vis-à-vis Russia, will prevent the continuation of strong bilateral dependencies [33]. The broad range of countries that emerge as potential exporters of green hydrogen (including Norway, Australia, New Zealand, Chile, and MENA),[34] implies not only that there is the prospect for supply chain diversification, but also that Europe’s dependence on authoritarian regimes can be lessened. Moreover, we are likely to witness a decrease in pressure on geographical areas vital to trade in fossil fuels (e.g., Hormuz Strait) and transit countries (e.g., Ukraine) [35]. Nevertheless, while the intensity of European foreign dependencies may thus be mitigated, value chains for hydrogen become more multi-layered as they involve raw materials, hydrogen technology, and components: for instance, whereas wind and solar required for green hydrogen are not regionally concentrated, this is however the case for nickel or platinum [36].

Secondly, as cheap costs of renewable electricity and the proximity of hydrogen production sites to the site of its use will determine production geographies, [37] Europe’s neighborhood and in particular North Africa once again, will be critical for supply to the EU [38]. Germany has already entered into a cooperation with Morocco, aiming to lay the foundations for future hydrogen exports [39]. Besides, the EU Commission’s Hydrogen Strategy emphasizes the importance of North Africa as “a potential supplier of cost-competitive renewable hydrogen to the EU” and further mentions Ukraine and the Western Balkans as potential partners [40]. Against the backdrop of more regionalized hydrogen supplies, the EU may be able to impose its own standards more effectively than in the case of fossil energies.

Lastly, it is imperative to stress the role of industrial policy. As Jermalavičius et al. argue, “the geopolitics of hydrogen will be about […] leveraging knowledge and innovation networks and access to hydrogen technology; about the ability to protect those technologies from geopolitical adversaries; and about […] ensuring security of supply of key raw materials […]” [41]. This fits the description of the geopolitics of green energy revolving around issues of “stocks” (i.e., raw materials, technology etc.), rather than the issue of “flows” which had been characteristic of the hydrocarbon age [42]. With the advent of “the era of a big race for technological leadership” in the hydrogen sector, as a recent IRENA report put it, [43] governments will increasingly step-up industrial policy in order to secure access to these “stocks”. In the EU the issue of industrial policy is particularly salient in the face of Chinese firms producing hydrogen technology such as electrolyses at much lower costs and the fact that countries that develop pioneering technologies (such as in fuel cells, storage tanks, pipeline materials or burners) will emerge as key suppliers for the global market [44].

Securing Critical Raw Materials for a Sustainable Transition

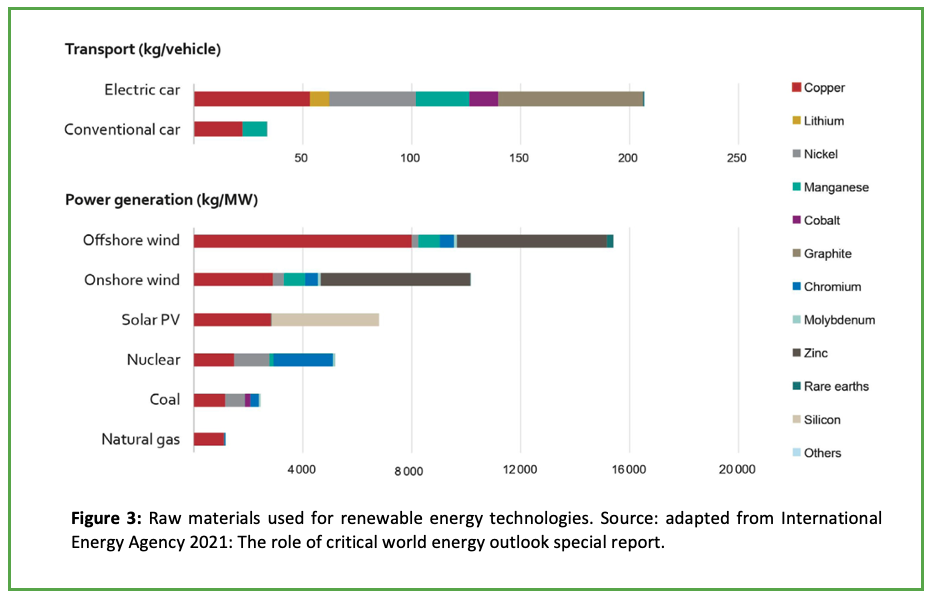

While hydrogen is recognized as a strategic technology for the green transition, critical raw materials (CRMs) are equally essential to achieving the EU’s climate objectives, sparking an intense global competition to secure these resources [45]. As illustrated by Figure 3, CRMs are vital for constructing wind turbines, solar panels, and electric vehicle batteries—all integral to Europe’s path toward climate neutrality [46]. Indeed, the EGD strategy will inevitably drive up the demand for CRMs, with projections indicating an increase from 7.5 million tons to as much as 28-43 million tons annually, depending on the scenario [47].

Securing access to these materials is thus imperative for achieving EU strategic autonomy in the 21st century [48].

The EU classifies 34 materials as CRMs, which include Lithium, Copper, or rare earth elements [49]. Demand for these resources will continue to grow in the future, as Europe and the rest of the world advance towards decarbonization and the digital economy [50]. For example, under a 2050 global carbon-neutrality scenario, demand for lithium could rise by as much as 175% [51]. Despite these prognoses, the EU currently remains highly dependent on imports for many CRMs, sourcing nearly all its heavy rare earth elements from China and 78% of its lithium from Chile (Figure 4) [52].

These dependencies will be further exacerbated by Europe’s climate ambitions and rising demand in other major economies undergoing the same transitions, which will seek to secure their own supply [53].

On this basis, concerns about the potential weaponization of CRMs are intensifying, especially in the case of China – which already demonstrated its willingness to restrict exports for diplomatic tensions, with the 2010 ban on rare earths to Japan [54]. Importantly, not only does China dominate certain mineral extractions, but it is also a leader in processing, refining 94% of Australian lithium before export [55]. However, Japan’s response to the 2010 ban – that led to the lowering of rare earths imports from 91% in 2008 to 58% by 2018 [56] – indicates that reducing reliance on China is not only crucial but also feasible.

Not the least after Russia’s invasion of Ukraine and the weaponization of natural gas, the EU has passed the Critical Raw Materials Act (CRMA) in 2024 to attempt to address its resource dependency challenges. This legislation in fact aims to significantly reduce the EU’s reliance on foreign actors for CRMs by 2030, with targets of extracting 10% of European annual demand domestically, processing 40% within the EU, and sourcing 25% from recycling. Additionally, the CRMA mandates that no single supplier should account for more than 65% of any material’s supply [58]. Concerningly however, the act does not envision any new funding from the EU budget to achieve these goals, neither for resource extraction nor for processing [59]. At the same time, the Commission is eager to bring producers and consumers of CRMs together in a “Club” and test out alternative trade arrangements [60].

Overall, it is clear that to address the issues related to CRM, the EU must diversify its imports and secure new partnerships in both resource extraction and processing. Simultaneously, it could also attempt to extract and process more CRMs domestically [61]. Large untapped deposits can be found in Sweden and the Danish territory of Greenland for instance, but opening mines and building up a whole processing supply chain is a lengthy process that can take decades [62]. The CRMA is thus undoubtedly a step in the right direction, but without funding and a coherent EU-wide strategy it risks becoming a paper tiger.

II. Global Implications: The EU as a Green Leader and Standard Setter

Through the EGD, the EU is positioned as a global leader in climate action, [63] aiming to transform its economy and to influence global environmental governance – which often relies on voluntary commitments or lacks robust enforcement, as exemplified by the Paris Agreement and the UN SDGs. Considering this, the EU can thus leverage its pioneering position in environmental legislation to affirm itself as a standard setter and a credible diplomatic actor on a global scale. Indeed, through its leadership by example it can initiate a ‘leader-laggard’ dynamic, whereby the high standards it establishes internally under the EGD generate international repercussions, prompting countries that lag behind in environmental policies to adopt more ambitious environmental targets [64]. Hence, as the EU pursues its ambitious climate goals, the EGD external dimension is crucial in determining how these efforts spread across borders and influence standards and policies abroad [65]. In a sense, this is evidence of the so-called “Brussels effect” in the domain of climate legislation [66].

Broadly, there are three main reasons why the EU pushes international actors towards more ambitious environmental policies:

- Achieving global standards requires cooperation: the EU’s internal efforts alone are insufficient to tackle the global climate crisis. Climate change does not stop at borders, and without other major economies adopting ambitious policies, global tipping points won’t be avoided [67]. The EU therefore engages in bilateral and multilateral climate diplomacy, using tools like trade agreements and foreign aid [68].

- Leadership as a strategic advantage: setting high environmental standards allows the EU to drive innovation and gain a strategic advantage in green technologies, boosting both its economic competitiveness and geopolitical influence. It sets benchmarks that other nations must meet if they want to trade with or invest in the EU [69].

- Avoiding competitive disadvantages: if other countries don’t follow suit, European industries may face higher costs, eventually leading to carbon leakage [70].

In practice, the EU’s efforts to “export the EGD” have also resulted in two initiatives that, while carrying considerable implications for global supply chain and trade patterns, are regarded as having the potential of scaling up sustainable practices world-wide.

Firstly, the Carbon Border Adjusted Mechanism (CBAM), which came into effect on October 1st, 2023. As a response to the risk of carbon leakage by companies outsourcing their production abroad so as to avoid the financial burden of the ETS, the EU developed an instrument that adjusts the prices of certain imported goods according to the carbon output emissions resulting from their productions. While addressing concerns on the EU’s potential competitiveness losses due to its carbon taxation, the CBAM was conceived as a tool able to stimulate the introduction of carbon pricing schemes among many of the EU’s trading patterns.

Secondly, the EU has adopted an anti-deforestation regulation (EUDR) [71]. Entered into force on June 29th, 2023, it prohibits the placement on the EU market or the export of products – such as cocoa, soy, palm oil, coffee, and certain derivatives – if they have contributed to deforestation or forest degradation [72]. The regulation’s considerable implications range from the reorientation of EU’s imports from high to low-risk jurisdictions – specifically, to countries that have stricter regulations in place – to the incentivization of anti-deforestation commitments by producers in order to continue exporting on the EU market [73]. Overall, this is expected to contribute to curb GHG emissions on a planetary scale, accelerating the reach of environmental goals globally.

Conclusion

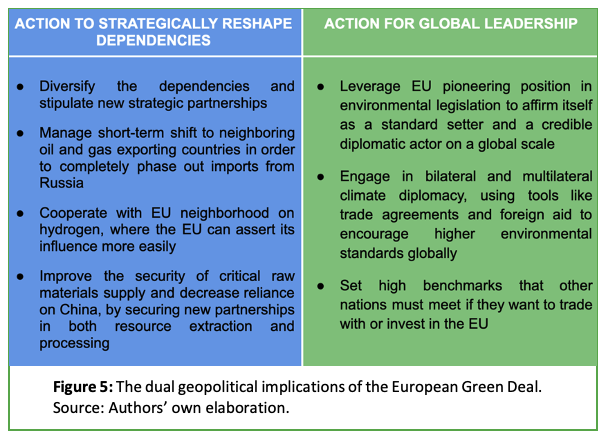

In conclusion, this paper has assessed the geopolitical implications embedded within the EU’s strategy to achieve climate neutrality by 2050. A synthesis of our findings is illustrated by Figure 5, that pictures the dual geopolitical repercussions of the EGD as per our investigation.

On the one hand, our analysis has demonstrated how the transition from fossil fuel dependency to renewable energy sources is neither immediate nor without challenges. As a matter of fact, Europe now confronts new potential dependencies, particularly concerning hydrogen, critical raw materials, and green technologies. However, our paper has also highlighted how the EU is now actively working to shape these new dependencies through a more strategic and long-term oriented approach, ensuring diversification and avoiding reliance on a limited set of untrustworthy global suppliers. While this increased awareness about dangerous dependencies is commendable, whether the EU will eventually succeed in this endevour remains to be seen.

On the other hand, we have also assessed how within the framework of the EGD, the EU acknowledges that international engagement is essential to achieving global sustainability objectives. Consequently, the Union is clearly positioning itself as a leader in global environmental governance. This leadership is crucial because it means that by establishing ambitious environmental standards, not only does the EU prevent harmful carbon leakage practices, but it is also able to influence global trade and environmental practices through its normative power. Against this background, the EGD emerges as more than just an environmental strategy: it is a comprehensive geopolitical framework that positions Europe at the forefront of the global race towards a sustainable future.

References

[1] Leonard, M., Pisani-Ferry, J., Shapiro, J., Tagliapietra, S., and Wolff, G. 2021. “The geopolitics of the European Green Deal.” Policy Contribution 04/2021, Bruegel. Accessed October 27, 2024 https://www.bruegel.org/system/files/wp_attachments/PC-04-GrenDeal-2021-1.pdf

[2] Marhold, Anna-Alexandra. 2023. “Towards a ‘Security-Centred’ Energy Transition: Balancing the European Union’s Ambitions and Geopolitical Realities.” Journal of International Economic Law 26 (December): 756–769. Accessed October 27, 2024. https://doi.org/10.1093/jiel/jgad043.

[3] Bjerkem, J. and Harbour, M. 2020. “Europe as a global standard-setter: The strategic importance of European standardisation.” Discussion Paper, Europe’s Political Economy Programme. European Policy Centre. Accessed October 27, 2024

https://www.epc.eu/content/PDF/2020/EPE_JB_Europe_as_a_global_standard-setter.pdf [

[4] ibid n. 1

[5] ibid n. 2

[6] Bolduc, Nathalie, Adis Dzebo, Alexia Faus Onbargi, Gabriela Ileana Iacobuţă, Niels Keijzer, and Daniele Malerba. July 2022. The European Green Deal and the War in Ukraine: Addressing Crises in the Short and Long Term. European Think Tanks Group. Accessed October 27, 2024. https://ettg.eu/wp-content/uploads/2022/07/The-European-Green-Deal-and-the-war-in-Ukraine.pdf,

[7] Ibid n. 2

[8] Quitzow, Rainer, and Yana Zabanova. “Introduction.” In The Geopolitics of Hydrogen, Volume 1: European Strategies in Global Perspectives, edited by Rainer Quitzow and Yana Zabanova, 3–4. Cham: Springer, 2024.

[9] Shi, Mingming, and Hannes Dekeyser. “Rare Earths Elements and Other Critical Raw Materials: A Geopolitical Headache for the EU.” Mercator Institute for China Studies (MERICS), 2023. Accessed October 27, 2024. https://merics.org/en/comment/rare-earths-elements-and-other-critical-raw-materials-geopolitical-headache-eu.

[10] Ibid n. 3

[11] Almeida, Diana Vela; Kolinjivadi, Vijay; Ferrando, Tomaso; Roy, Brototi; Herrera, Héctor; Vecchione Gonçalves, Marcela; Vam Hecken, Gert. 2023. The “Greening” of Empire: The European Green Deal as the EU first agenda. Political Geography, 105 ISSN 0962-6298. Accessed October 27, 2024 https://doi.org/10.1016/j.polgeo.2023.102925.

[12] International Renewable Energy Agency (IRENA). 2019. “A New World: The Geopolitics of the Energy Transformation.” Accessed October 27, 2024. https://www.irena.org/-/media/files/irena/agency/publication/2019/jan/global_commission_geopolitics_new_world_2019.pdf.

[13] Marhold, Anna-Alexandra. 2023. “Towards a ‘Security-Centred’ Energy Transition: Balancing the European Union’s Ambitions and Geopolitical Realities.” Journal of International Economic Law 26 (December): 756–769. Accessed October 27, 2024. https://doi.org/10.1093/jiel/jgad043.

[14] Ibid. n 3 (p. 759).

[15] Cretti, Giulia, Akash Ramnath, and Louise Van Schaik. October 2022. “Transitioning Towards Energy Security Beyond EU Borders: Why, Where and How?” Policy Brief, Clingendael Netherlands Institute of International Relations. Accessed October 27, 2024. https://www.clingendael.org/sites/default/files/2022-10/Policy_brief_Transitioning_towards_energy_security_beyond_EU_borders.pdf.

[16] Bolduc, Nathalie, Adis Dzebo, Alexia Faus Onbargi, Gabriela Ileana Iacobuţă, Niels Keijzer, and Daniele Malerba. July 2022. The European Green Deal and the War in Ukraine: Addressing Crises in the Short and Long Term. European Think Tanks Group. Accessed October 27, 2024. https://ettg.eu/wp-content/uploads/2022/07/The-European-Green-Deal-and-the-war-in-Ukraine.pdf, p. 7.

[17] Guarascio, Dario, Reljic Jelena, and Francesco Zezza. 2024. “Assessing EU Energy Resilience and Vulnerabilities: Concepts, Empirical Evidence and Policy Strategies.” OFSE Working Paper No. 77. Accessed October 27, 2024. https://www.econstor.eu/bitstream/10419/300845/1/1897699417.pdf, p. 13.

[18] Siddi, Marco. 2023. “Next Steps for the European Green Deal: Navigating Economic and Security Challenges, Keeping a Focus on Climate and Justice.” Trans-European Policy Studies Association. May 3. Accessed October 27, 2024. https://tepsa.eu/analysis/next-steps-for-the-european-green-deal-navigating-economic-and-security-challenges-keeping-a-focus-on-climate-and-justice/.

[19] Ibid. n. 15

[20] European Commission. 2022. “EU External Energy Engagement in a Changing World.” May 18.

[21] European Commission. May 2024. “REPowerEU – 2 Years On.” Accessed October 27, 2024. https://energy.ec.europa.eu/topics/markets-and-consumers/actions-and-measures-energy-prices/repowereu-2-years_en#:~:text=Reducing%20gas%20demand&text=Natural%20gas%20demand%20declined%20by,avoid%20blackouts%20and%20power%20shortages.

[22] European Union Agency for the Cooperation of Energy Regulators (ACER). April 19, 2024. “Analysis of the European LNG Market Developments: 2024 Market Monitoring Report.” Accessed October 27, 2024. https://www.acer.europa.eu/sites/default/files/documents/Publications/ACER_2024_MMR_European_LNG_market_developments.pdf.

[23] Ibid. n 10.

[24] Ibid. n 22.

[25] European Council Conclusions. EUCO 31/22, 20 and 21 October 2022.

[26] European Commission. “AggregateEU – Questions and Answers.” Accessed October 27, 2024. https://energy.ec.europa.eu/topics/energy-security/eu-energy-platform/aggregateeu-questions-and-answers_en.

[27] Council of the European Union. “EU Gas Supply.” Accessed October 27, 2024. https://www.consilium.europa.eu/en/infographics/eu-gas-supply/.

[28] Leonard, Mark, Guy Meunier, Simone Tagliapietra, Georg Zachmann, and Guntram B. Wolff. “A European Green Deal for Industry: Addressing Competitiveness, Investment, and Carbon Leakage.” Bruegel Policy Contribution 04/2021. 2021. Accessed October 27, 2024. https://www.bruegel.org/system/files/wp_attachments/PC-04-GrenDeal-2021-1.pdf.

[29] Ibid. n 28.

[30] Quitzow, Rainer, and Yana Zabanova. “Introduction.” In The Geopolitics of Hydrogen, Volume 1: European Strategies in Global Perspectives, edited by Rainer Quitzow and Yana Zabanova, 3–4. Cham: Springer, 2024.

[31] Ibid. n. 30 (p. 6).

[32] Van de Graaf, Thijs, et al. “The New Oil? The Geopolitics and International Governance of Hydrogen.” Energy Research & Social Science 70 (2020).

[33] Jermalavičius, Tomas, et al. “European Hydrogen Dreams.” In Geopolitics of Europe’s Hydrogen Aspirations: Creating Sustainable Equilibrium or a Combustible Mix? International Centre for Defence and Security (ICDS), 2022, 2–10.

[34] Ibid. n 32.

[35] Ibid. n 32.

[36] Pepe, Jacopo Mari, et al. The Geopolitics of Hydrogen: Technologies, Actors, and Scenarios until 2024. SWP Research Paper, Stiftung Wissenschaft und Politik/German Institute for International and Security Affairs, 2023, 6–8.

[37] Ibid. n 30 (p. 5).

[38] Ibid. n 28 (p. 6).

[39] Bundesministerium für Wirtschaft und Klimaschutz. “Deutschland und Marokko vereinbaren Allianz für Klima und Energie.” Berlin: Bundesministerium für Wirtschaft und Klimaschutz, 2024. https://www.bmwk.de/Redaktion/DE/Pressemitteilungen/2024/06/20240628-deutschland-marokko-allianz-fuer-klima-und-energie.html#:~:text=Bereits%20jetzt%20beteiligt%20sich%20Deutschland,Tonnen%20grünen%20Stahl%20zu%20produzieren.

[40] European Commission. A Hydrogen Strategy for a Climate-Neutral Europe. COM(2020) 301 final. 2020. Accessed October 27, 2024. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0301.

[41] Ibid. n 33 (p. 9).

[42] E3G & Stanley Center for Peace and Security. The Geopolitics of the Energy Transition and Opportunities for International Cooperation: Readout & Recommendations. 2023, 2.

[43] International Renewable Energy Agency (IRENA). Geopolitics of the Energy Transformation: The Hydrogen Factor. Abu Dhabi: 2022, 14.

[44] Ibid. n. 32.

[45] Hein, Andreas, and Jakob Lykke Pedersen. “The EU’s Critical Raw Materials Act: Enhancing Security of Supply for Europe.” Hertie School Jacques Delors Centre, 2023. Accessed October 27, 2024. https://www.delorscentre.eu/en/publications/eu-critical-raw-materials.

[46] Shi, Mingming, and Hannes Dekeyser. “Rare Earths Elements and Other Critical Raw Materials: A Geopolitical Headache for the EU.” Mercator Institute for China Studies (MERICS), 2023. Accessed October 27, 2024. https://merics.org/en/comment/rare-earths-elements-and-other-critical-raw-materials-geopolitical-headache-eu.

[47] Geopolitical Intelligence Services. “Sweden’s Critical Materials Are Key for Europe.” GIS Reports Online, 2023. Accessed October 27, 2024. https://www.gisreportsonline.com/r/sweden-critical-materials-europe/.

[48] Rossetto, Nicolo, Marzia Sesini, and Max Munchmeyer. “The Green Deal Industrial Plan.” Florence School of Regulation, European University Institute, 2023. Accessed October 27, 2024. https://fsr.eui.eu/the-green-deal-industrial-plan/.

[49] Deloitte. “The Critical Raw Materials Act and Its Geopolitical Implications.” Deloitte Central Europe, 2023. Accessed October 27, 2024. https://www.deloitte.com/ce/en/related-content/the-critical-raw-materials-act-and-its-geopolitical-implications.html.

[50] Ibid. n. 48.

[51] Ibid. n. 48.

[52] Ibid. n. 48 (p. 3).

[53] Ibid. n. 45 (p. 1).

[54] Tagliapietra, Simone, and Guntram B. Wolff. “Why Europe’s Critical Raw Materials Strategy Has to Be International.” Bruegel, 2023. Accessed October 27, 2024. https://www.bruegel.org/analysis/why-europes-critical-raw-materials-strategy-has-be-international (p. 2).

[55] Ibid. n. 54 (p. 5).

[56] García, Juan Carlos. “Geopolitical Risk, Raw Materials, and Technological Dependence.” Real Instituto Elcano, 2023. Accessed October 27, 2024. https://www.realinstitutoelcano.org/en/commentaries/geopolitical-risk-raw-materials-and-technological-dependence/.

[57] Ibid. n. 54 (p. 1).

[58] Ibid. n. 48.

[59] Ibid. n. 45 (p. 2).

[60] Ibid. n. 45 (p. 2).

[61] Ibid. n. 45 (p. 4).

[62] Geopolitical Intelligence Services. “Sweden’s Critical Materials Are Key for Europe.” GIS Reports Online, 2023. Accessed October 27, 2024. https://www.gisreportsonline.com/r/sweden-critical-materials-europe/.

[63] European Commission. The European Green Deal. COM (2019) 640 final. Brussels, December 11, 2019. Accessed October 27, 2024. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52019DC0640.

[64] Bulmer, Simon, et al. (2005). “Policy Transfer in the European Union: An Institutionalist Perspective.” British Journal of Political Science 35 (1): 103–126.

[65] Koch, S. and Keijzer, N. 2021. “The external dimensions of the European Green Deal: The case for an integrated approach.” Briefing Paper (13/2021), German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE). Accessed October 27, 2024. https://www.idos-research.de/uploads/media/BP_13.2021.pdf

[66] Bradford, A. 2020. The Brussels Effect: How the European Union Rules the World. New York: Oxford Academic. Accessed October 27, 2024. https://doi.org/10.1093/oso/9780190088583.001.0001

[67] Lafortune, G., Fuller, G., Kloke-Lesch, A., Koundouri, P., and Riccaboni, A. 2024. European Elections, Europe’s Future and the SDGs: Europe Sustainable Development Report 2023/24. Paris: SDSN and SDSN Europe; Dublin: Dublin University Press. Accessed October 27, 2024. https://s3.amazonaws.com/sustainabledevelopment.report/2024/europe-sustainable-development-report-2023-24.

[68] Council of the European Union. “Climate External Policy.” Accessed October 27, 2024. https://www.consilium.europa.eu/en/policies/climate-change/climate-external-policy/

[69] Bjerkem, J. and Harbour, M. 2020. “Europe as a global standard-setter: The strategic importance of European standardisation.” Discussion Paper, Europe’s Political Economy Programme. European Policy Centre. Accessed October 27, 2024. https://www.epc.eu/content/PDF/2020/EPE_JB_Europe_as_a_global_standard-setter.pdf

[70] Leonard, M., Pisani-Ferry, J., Shapiro, J., Tagliapietra, S., and Wolff, G. 2021. “The geopolitics of the European Green Deal.” Policy Contribution 04/2021, Bruegel. Accessed October 27, 2024. https://www.bruegel.org/system/files/wp_attachments/PC-04-GrenDeal-2021-1.pdf

[71] European Commission. Regulation (EU) 2023/1115 of the European Parliament and of the Council of 14 June 2023 Establishing a Framework for the Development of the European Union’s Critical Raw Materials Policy. Brussels, 2023. Accessed October 27, 2024. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32023R1115.

[72] French Ministry of Ecological Transition. “The European Deforestation-Free Regulation.” Accessed October 27, 2024. https://www.deforestationimportee.ecologie.gouv.fr/en/the-european-deforestation-free-regulation/article/the-european-deforestation-free-regulation.

[73] S&P Global. “The Global Impact of the EU’s Anti-Deforestation Law.” Accessed October 27, 2024. https://www.spglobal.com/esg/insights/featured/special-editorial/global-impact-of-the-eu-s-anti-deforestation-law.